Case study: A strategic planning conference for a veterinary practice

Think you don't have time for strategic planning? Check out this case study, which shows how one practice used a year-end review to plan for next year's success. You just might find the time after all.

Lake Hope Veterinary Center (LHVC) is a seven-doctor practice co-owned by Drs. Linzell and Davis. The practice holds an annual two-day strategic planning conference, facilitated by a management consultant, in December at a local hotel and conference center. Attendees include the practice manager, the financial and compliance manager, the IT manager, and the reception and technician team leaders. One of the practice's associates, Dr. Rose, is on the partner track and participated for the first time this year. Here are the results from this year's conference.

A CLOSER LOOK

The agenda

Here's an overview of the LHVC team meeting.

1. Review vision statement and mission statement and modify as necessary. Based on the discussions, the group decided to keep their existing vision statement and to modify their mission statement.

> Existing vision statement: "Happy, healthy pets and cheery, satisfied clients."

> New mission statement: "We preserve and protect our patients' health and nurture our client relationships."

2. Discuss the past year's accomplishments. Each segment of the management team presented a list of the group's achievements during 2011 (see "The accomplishments").

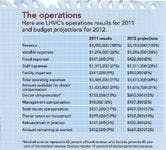

3. Review the practice's operations in 2011. The financial manager presented the annualized results of operations (see "The operations").

The operations

4. Perform a SWOT analysis. The group developed a list of LHVC's strengths, weaknesses, opportunities, and threats (SWOT) and then developed goals and an action plan for 2012 based on their analysis. Together with the consultant, the group settled on the following:

GOAL 1: Update the LHVC operating and shareholder agreements.

> Drs. Linzell and Davis will review the existing agreements, which function as organizational documents that stipulate how the business will operate. They are reviewed every three to five years. Drs. Linzell and Davis have decided to review the agreements ahead of Dr. Rose's buy-in to make any necessary changes. They'll discuss possible changes on January 10, and again in 2014, when Dr. Rose buys in.

> Drs. Linzell and Davis will meet with their attorney on January 20 to discuss and seek input on the changes.

> The attorney will update the documents by March 15.

GOAL 2: Plan for Dr. Rose's buy-in with a target date of 2014.

> Continue to mentor Dr. Rose, discussing "Building blocks that create successful owners" and "Topics to discuss before becoming partners" from Benchmarks 2010: A Study of Well-Managed Practices (see dvm360.com/benchmarks2010).

> Delegate responsibility for the practice's medical development plan to Dr. Rose (see "Always look ahead" below). Explain to her the responsibilities, resources available, and time necessary for this management project. Dr. Rose will receive 10 percent of the management fee, or $10,000, for her management responsibilities.

> Drs. Linzell, Davis, and Rose will attend the Veterinary Economics Progress in Practice valuation workshop at CVC Washington D.C. in April.

> Work with the practice's management consultant to identify opportunities to improve profit and value.

> Value the practice in December 2012 for planning purposes.

GOAL 3: Review and approve 2012 budget.

> Institute a fee increase of 3 percent on non-shopped services (projected revenue: $100,000).

> Recapture missed charges (projected revenue: $50,000).

> Focus on improved healthcare compliance in key areas of six-month exams, wellness lab work, fecal testing, and dentistry (projected revenue: $200,000).

> Add new services (see Goal 4) (projected revenue: $100,000).

> Reduce inventory cost (projected savings: $70,000).

> Reduce the amount of outsourced IT support (projected savings: $13,000).

> Offer pay increases to existing team members and hire two additional receptionists and two additional technicians (projected cost: $198,100).

GOAL 4: Add new services in 2012

> Add laser therapy (Dr. Rose).

> Add rehabilitation therapy (Dr. Davis).

> Add acupuncture (Dr. Linzell).

GOAL 5: Hold quarterly strategic planning conferences in 2012.

> Schedule one-day conferences in March, June, and September.

> Discuss progress with implementation of annual action plan.

> Modify annual action plan if necessary based on implementation results.

> Schedule the practice's next two-day annual conference in December.

What's the difference between a vision and mission statement?

A vision statement defines the way an organization looks to the future. Vision is a long-term view, sometimes describing how the organization would like the world to be. Example: "A world without poverty." A mission statement is a company's purpose. The mission guides the actions of the organization, spells out its overall goal, provides a path, and influences decision-making. It provides the framework within which the company's strategies are formulated. Example from Google: "We organize the world's information and make it universally accessible and useful."

Always look ahead

As a veterinary practice owner, you must ensure that all employees have the medical knowledge they need to work efficiently, effectively, and productively. Visit dvm360.com/medicaldevelopment for a plan to help your team keep up with the times.

The accomplishments

Here's a look at what each team member at Lake Hope Veterinary Center achieved this year.

PRACTICE OWNERS

Successfully implemented weekly management team meetings. → Developed technician CE programs (with input from technician team leaders) marketed to area practices as an opportunity for local high-quality, cost-effective education. → Completed acupuncture certification (Dr. Linzell) and rehabilitative therapy certification (Dr. Davis). → Began mentoring Dr. Rose in the business side of the practice.

DR. ROSE

Began participating in the weekly management team meetings. → Attended the Veterinary Economics Progress in Practice Workshop at CVC Kansas City to gain a better understanding about the financial side of the practice. → Helped develop a plan to reduce inventory costs in 2012. → Began reading management books and publications provided by Dr. Linzell.

PRACTICE MANAGER

Updated the Lake Hope Veterinary Center employee manual. → Developed customized training and education schedules for each team member. → Mapped out the practice's CE plan for 2012. → Helped prepare the budget for 2012. → Helped develop a plan to reduce inventory costs in 2012.

FINANCIAL MANAGER

Successfully met the 2011 budget in all categories except inventory cost. → Helped develop a plan to reduce inventory costs in 2012. → Developed the 2012 budget (approval pending). → Compiled a monthly financial management workbook for the owners' use (see "To do").

IT MANAGER

Set up an internal e-mail account for each doctor and team member to facilitate improved communication. → Upgraded the network server and select hardware. → Installed the latest updates for the practice management software. → Established additional internal control protections for practice management software.

RECEPTION TEAM LEADERS

Helped develop the reception training and education schedules, as well as the CE plan for 2012. → Terminated a receptionist who wasn't happy in her position and was creating challenges for other team members; successfully hired a replacement. → Developed a receptionist CE program to market to area practices as an opportunity for local high-quality, cost-effective education (approval pending). → Submitted a request to hire two additional receptionists in 2012 to further strengthen customer service (approval pending).

TECHNICIAN TEAM LEADERS

Helped develop the technician training and education schedules, as well as the CE plan for 2012. → Terminated two technicians who weren't happy in their positions and were creating challenges for other team members; successfully hired replacements. → Helped develop the technician CE programs marketed to area practices. → Submitted a request to hire two additional technicians to assist with the new services that LHVC plans to add in 2012 (approval pending). → Helped develop a plan to reduce inventory costs in 2012.

MANAGEMENT SKILL-BUILDER

To do: Compile a financial management workbook

Veterinary practice owners need access to specific financial information each month to effectively manage their business and analyze practice performance. Ask your financial manager or bookkeeper to provide the following reports by the 20th of each month to provide a timely financial picture:

> Balance sheet and profit-and-loss statement from your accounting software.

> Management statement (see "The management statement").

> Detail of owner draws (if applicable) and distributions.

> Inventory exception report.

> Accounts receivable aging by client, showing clients more than 60 days past due and clients sent to collection.

> Debt worksheet (include loan amortization schedules and schedules of future anticipated loan payment).

The management statement: Keep an eye on the money

This report monitors that all-important metric: cash flow.

Many veterinarians use their income statement as a management tool and come away frustrated. Income statements are designed to determine taxable income, not measure cash flow, and cash flow is the lifeblood of a practice. Convert your income statement to a management statement using these steps to monitor cash flow, profitability, and budget variances.

Group expenditures into categories by their impact on practice revenue.

Use a set of colored highlighters to separate each expense type on your practice's income statement.

1. Variable expenses: These are expenses directly affected by the number of patients seen—for example, drugs and supplies, laboratory expenses, and practice vehicles. Highlight in yellow.

2. Fixed expenses: Expenses that exist regardless of the number of patients seen. These are the costs that "keep the doors open," like telephone bills, repairs to office equipment, office supplies, and CE. Highlight in purple.

3. Staff compensation: Salaries, retirement contributions, and employer payroll taxes for non-doctor staff. Highlight in pink.

4. Non-owner veterinarian compensation: Salaries, retirement contributions, and employer payroll taxes for associates. Highlight in pink, but enter separately from staff compensation.

5. Owner compensation: Salaries, life and disability insurance, owner distributions, owner draws, and employer payroll taxes for owners. Highlight in pink, but enter separately from staff compensation and non-owner veterinarian compensation.

6. Facility expenses: The greater of rent payments, mortgage payments, or fair market rent, as well as property and casualty insurance, utilities, real estate taxes, and facility repairs and maintenance. Highlight in green.

7. Reinvestment in practice: Equipment purchases, loan or capital lease interest payments, equipment rental, and loan or capital lease principal payments. For some practices, some of these amounts will come from your balance sheet in addition to your income statement. Highlight in blue.

Calculate cash-basis profit.

The first measure of profit is the amount available for veterinarian compensation. This is the amount remaining after paying all variable, fixed, staff compensation, and facility expenses. It's the amount available for all veterinarians (owners and associates) and for reinvestment in the practice.

The second measure of profit is the amount available for reinvestment. This is calculated by subtracting associate compensation and practice owners' veterinary and management compensation from the amount available for veterinary compensation.

Summarize important revenue information.

Your revenue summary should include:

> Productivity by veterinarian (enter total revenue, number of transactions, and average charge per transaction).

> The number of active clients and the number of new clients for the current year and prior year. You can calculate client visitation by dividing the total medical transactions by total active clients. One estimate for calculating client retention is to divide total active clients by total new clients.

When you prepare this report regularly, you'll spot problems sooner rather than later. And you'll soon wonder how you functioned without this information.